#1 Starting The Journey Out of Debt

- The Crypto MD

- Dec 16, 2022

- 3 min read

Updated: Dec 19, 2022

December 2022: About me, my starting position and where to from here.

An anonymous medical finance blog... Hard to believe right? There are lots out there, we all know folks like The White Coat investor, Dev Raga etc. But, one person that inspired me was 'Dr Pay it back" on twitter (https://twitter.com/DrPayItBack) who is an anesthesiologist posting about their wins (and losses) while sharing financial progress since medical school. As it pertains to any of these folks, I think sharing the financial journey between medical professionals of all stages (student, intern, resident, fellow etc.) is useful. Certainly for me, it has helped build an understanding of where I am at, and whats to come. Since I was planning on tracking my personal finances and doing my best to get the hell out of debt, I figured doing it publicly (buy anonymously) would be nice. It can hopefully help others in the same position, and be a forum for people to share ideas and thoughts. This first post might be long, as it will dive a bit into my personal story for context on my financial history - as well as introduce my net position today, December 16, 2022 - at the end of my second year as a full-time doctor.

Click the twitter profile for a link to follow!

What my story?

Look, I don't want to tire you with some kind of sob story about my life. I just want to frame what money means to me, from my upbringing from a lower-middle class family to having mountains of post-secondary & medical school. The context is important in understanding why and who I am from a financial perspective. I come from a relatively poor family, both parents barley had high-school education. My mom is an immigrant to Canada, born abroad and never really holding steady prolonged employment. My dad was a mechanic who transitioned into the tech sector with some success. Ultimately, money was always a problem as a kid - I was told we never had any. Their stance is openly admitting to being 'bad with money'. I was the first person in my entire family line (including extended) to go to post-secondary education and thrive academically... The thought was foreign to my parents, and thus there was NO savings for me to go to school, no preparation... I was f*cked from jump-street financially - debt would be the only way to get an education.

Going to university for my Bachelors degree I would accumulate ~ $60,000 in provincial debt (OSAP Loan) - whoops...

To get my Master's I think I made a small amount of money given the fact that you get paid to research and teach, but after rent and living this was essentially negligible.

And then... There was medical school. I am a Canadian going who went to school in Australia. I don't want to explain why that is and what getting into medical school in Canada is like, but let's just say it's extremely competitive; I had a 4.0 GPA and above average MCAT - didn't even get an interview. Anyway, this would ultimately set me back to the tune of ~ $241,940 (Personal line of credit) at it's peak. At the time in 2017, the idea of a prime + 1% loan (which was ~ 2.4%), interest wasn't a huge issue. As we speak, my loan interest is 6.45%!! F*cked again.

My current position:

To quickly catch you up, I have managed to shave ~$40,000 off my total debt and add ~$80,000 to my assets. All while making an intern/resident salary of < $100,000 / year. I will explain how I did this in a future post going over my income sources and how I 'pay myself' with each pay slip. The main 2 ways I've managed to make this progress are: 1. Living like a medical student and 2. Cryptocurrency.

Yes, cryptocurrency. I will make a longer post about how I made money in Crypto, but just know that was a big part. Keep your judgement to yourself for now, I'm sure 95% of you will will probably say something like 'crypto is a scam'... But all I know is that I have significantly increased by net worth thanks to crypto so if it's a scam, then it's the best scam I've ever been part of. Thus, my name (The Crypto MD).

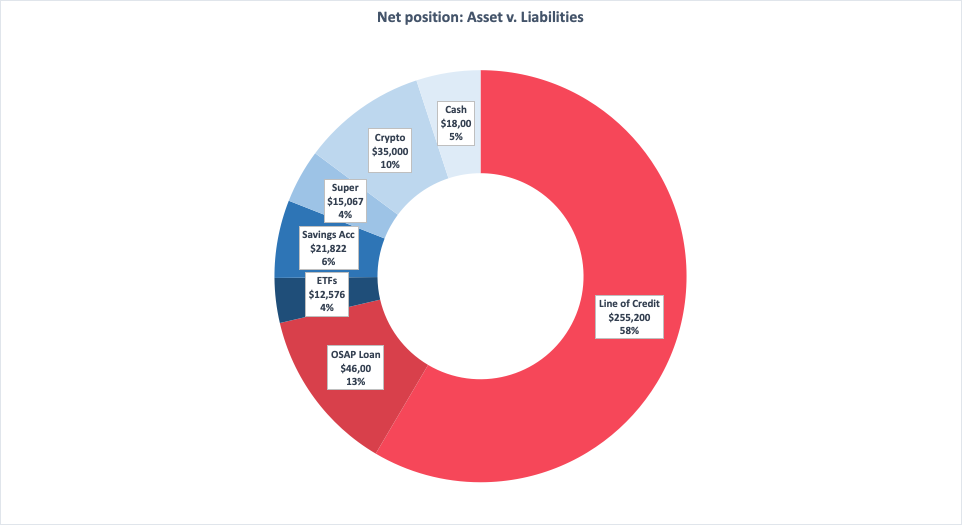

Starting position (01/2021) | Liability $295,086 | All Assets ~20,000 |

|---|---|---|

Current (12/2022) | Liability $255,200 | All Assets ~101,923 |

Breakdown of Current Liabilities (Dec 2022)

Personal Line of Credit | Provincial Student Loans |

-$ 209,200 | -$ 46,000 |

Interest: 6.45% | Interest: 3% Provincial only |

Breakdown of Current Assets (Dec 2022)

ETF & Stocks | Savings Account | Super Fund/RRSP | Cash | Cryptocurrency |

$12,576 | $21,822 | $15,067 | $17,457 | $~35,000 |

Largest holding: VTS (Vangaurd total US stock market) | Comm bank, Net Saver. Interest rate: 1.60% p.a. paid monthly | Aware Super, High-growth fund. | Largest holdings: Ethereum, Polkadot, Bitcoin. |

Moving forward

There is a lot more to my philosophy, story and plans. But for now I want to keep it short. I will keep posting every month to update you on my debt/wealth building process. I will also write some posts outlining how I save, invest, breakdown my pay slips etc.

In the mean time, give me a follow on twitter and tell me how stupid you think I am for owning cryptocurrency!

Happy Holidays

@ThecryptoMD

Comments